Why North American Ski Resorts Don't Invest in Lifts Like Europe Does

Published Date:

Melbourne-based skier and snowboarder with 50+ resorts across 5 continents. Specialises in Australian resorts and international resort comparisons.

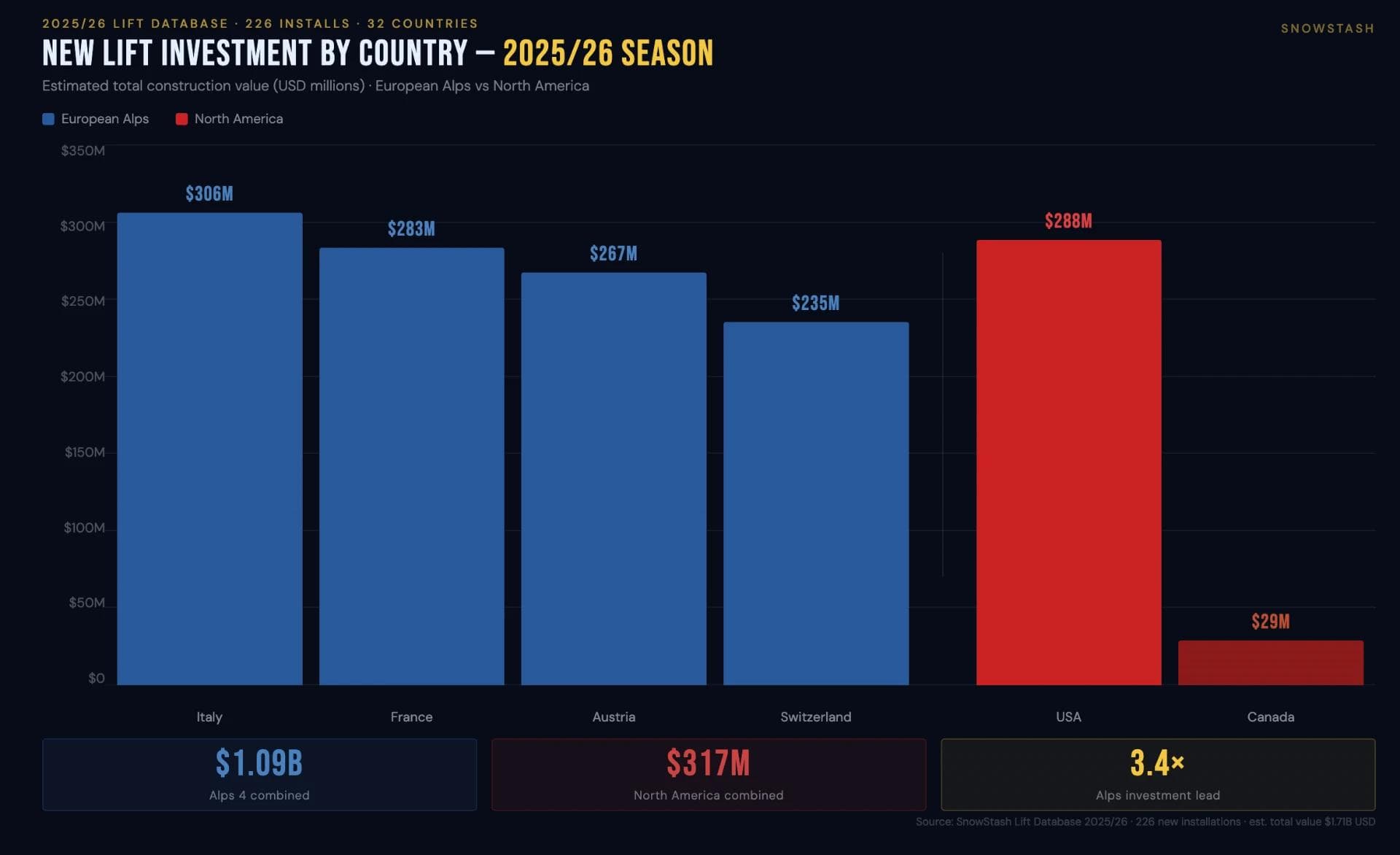

North American ski resorts spent $317 million on new lift infrastructure in the 2025/26 season. The four core Alpine nations - Italy, France, Austria, and Switzerland - spent $1.09 billion.

New Lift Investment 2025/26 Across Europe / North America

That's not a rounding error. That's a structural problem.

I've spent the past two seasons doing month-long trips through the Alps, and the lift infrastructure has been genuinely difficult to ignore. Not just the hardware, but the ambition - the scale of projects, the regularity with which resorts rip out perfectly functional lifts and replace them with something significantly better. Having also spent decent stretches in North America, the contrast kept nagging at me.

So I went looking for a proper answer. I built a complete database of all 226 new lift installations across 32 countries for the 2025/26 season, and a detailed financial comparative report covering European and North American operators across multiple seasons of audited data. The full report and the lift database are available to download below:

Global Ski Industry Comparative Report

New Ski Lift Globally 2025/2026

What I found is more interesting, and more structurally damning, than simply pointing at corporate greed.

The Real Reason American Ski Resorts Won't Upgrade Their Lifts

The numbers that frame the gap

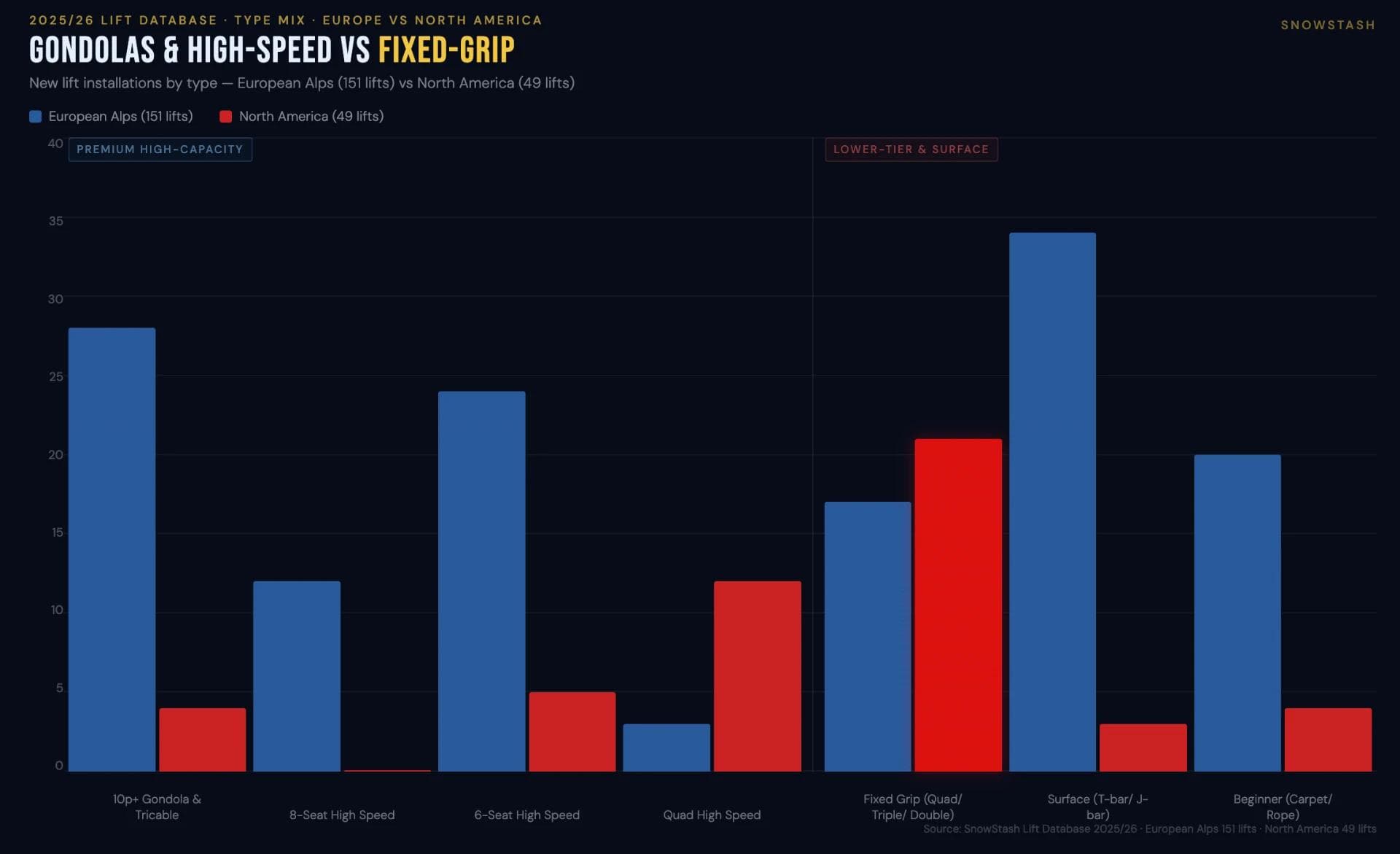

Total investment is only part of the picture. Cost per lift is where the divergence really shows. Switzerland averages $16.75 million per new lift installation. The US average is $6.85 million. The Swiss are building lifts that cost nearly two and a half times more per unit - not because Swiss mountains are inherently more expensive to build on, but because they're building fundamentally different products.

In 2025/26, Europe installed 27 new 10-person gondolas. North America installed four. Europe put up 12 new 8-seat high-speed detachable chairs. North America installed zero. The most common new lift type across North America was the fixed-grip quad - 14 of them, making up 28% of all North American installations for the season. A fixed-grip quad is reliable, functional, and the kind of lift you'd see highlighted in a resort brochure from the late 1980s.

A breakdown of the Lift Types that were installed in 2025/26

Three European projects from the database sit in a category of their own. The Campitello-Col Rodella 3S tri-cable gondola in Val di Fassa [internal link] came in at an estimated $39.9 million. The Schilthorn 100-seat Funifor aerial tram above Mürren [internal link] - yes, the James Bond one, yes the 29th-largest resort in Switzerland - cost an estimated $43.8 million, part of a multi-season, 200-million-euro valley-to-summit investment programme I actually got to ski during in January. And Hoch-Ybrig in Switzerland installed the world's first TRI-Line 20-seat tri-cable system at $32.2 million. None of these are flagship megastations. They're the normal replacement cycle.

It starts with who owns the mountain

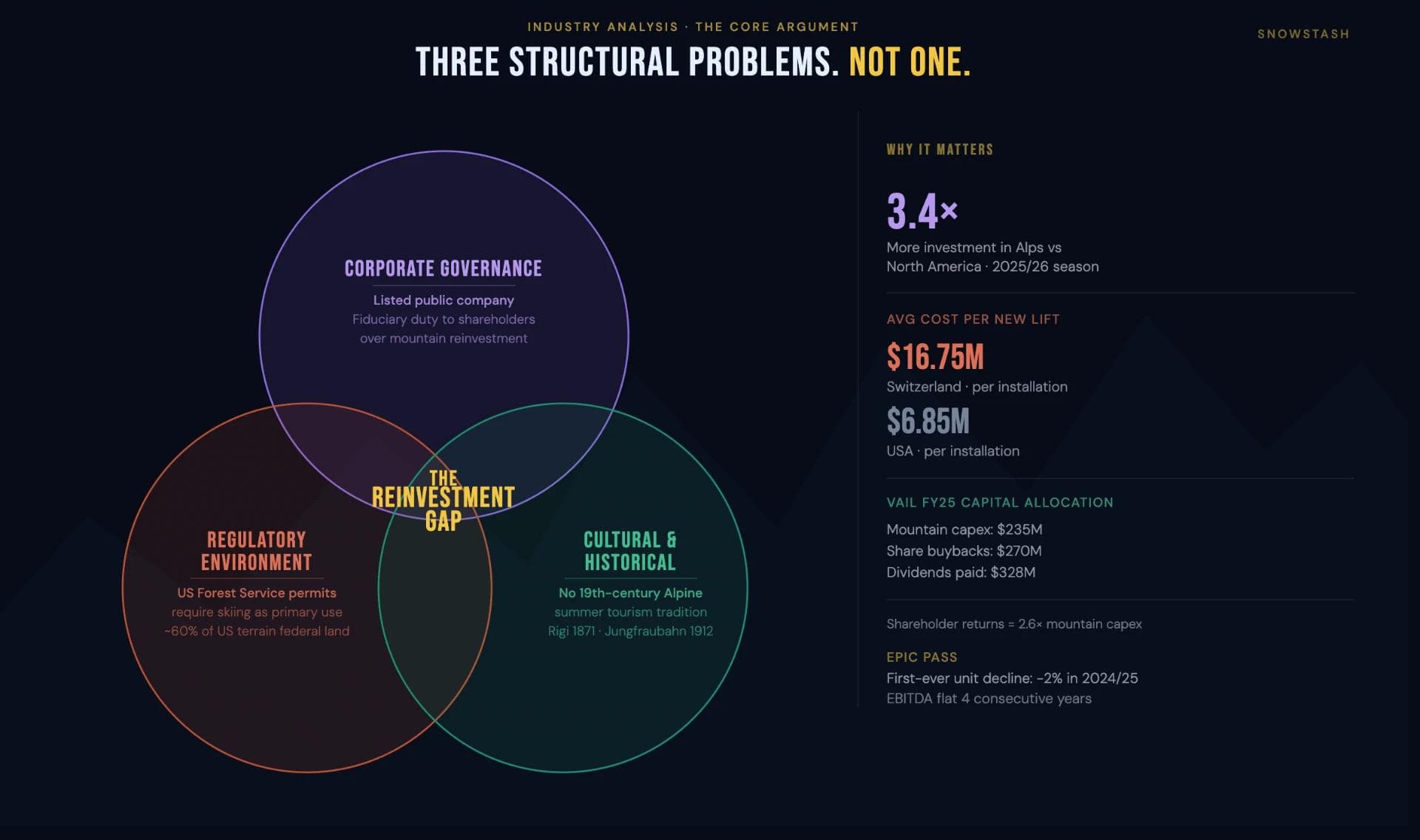

The ownership structure of a ski resort determines almost everything about how it spends money. That's not an abstraction - it's the single clearest lens for understanding this gap.

In North America, the dominant force is Vail Resorts, listed on the New York Stock Exchange and operating 42 resorts globally. In their 2025 financial year, they posted $844 million in EBITDA on $2.96 billion in revenue. Those are strong numbers by any measure.

The question is what happened to that $844 million. Mountain capex - actual physical investment in the resort experience - came to approximately $225 million, around 7.5% of revenue. Share buybacks accounted for $265 million. Dividend payouts ran at roughly $330 million annually. Total shareholder returns for the year: approximately $595 million. Total mountain investment: $225 million. Vail returned 2.6 times more to shareholders than it put back into its mountains.

This isn't illegal, and it isn't unusual for a publicly-listed company. The people running Vail are operating exactly as a listed company's governance model requires - maximising returns to shareholders. That is their fiduciary duty. The problem is the structure, not the individuals inside it.

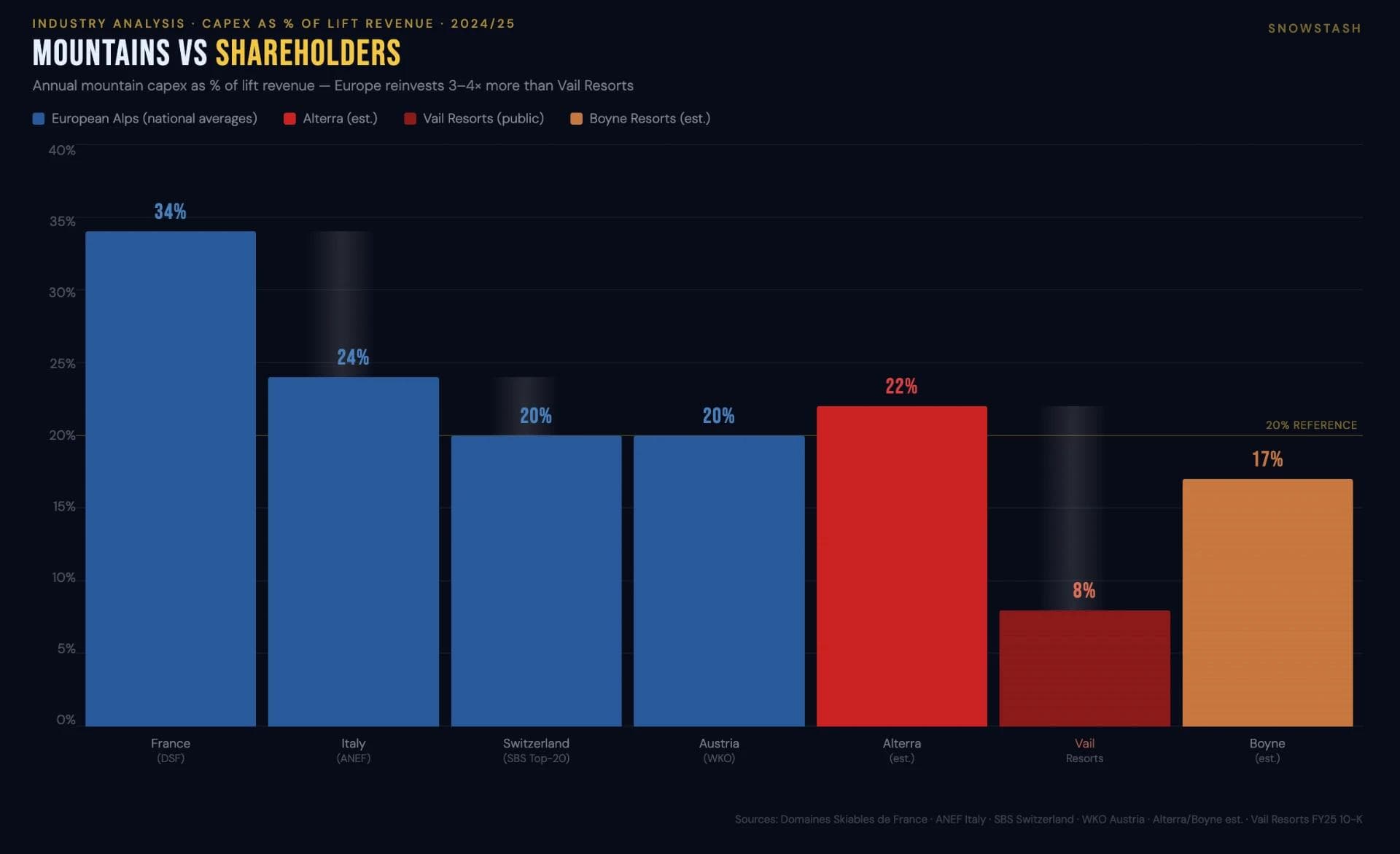

Contrast that with Europe. France's ski industry reinvests 34% of revenue in capex. Austria and Switzerland sit around 20%. Compagnie des Alpes, the largest publicly-listed European ski operator, spent €106 million in capex against €594 million in ski revenue - an 18% reinvestment rate, more than double Vail's.

Showing the difference of reinvestment across the major countries in the report.

The difference comes down to three ownership models that look nothing like the Vail model.

Austrian resorts are largely private AGs or GmbHs - private limited companies owned by families, local municipalities, or a combination. Bergbahn AG Kitzbühel is 49.93% owned by the local council. Silvrettaseilbahn AG at Ischgl is owned by the surrounding valley communities. There are no external shareholders demanding quarterly returns. The equity exists to fund the next infrastructure cycle. That's it.

French resorts operate under legislation from 1985 that legally classifies ski lift operation as a public industrial and commercial service. Local councils are the operating authority, either running lifts directly or granting a 25-year concession to a private operator. A 25-year operating guarantee completely changes what capital investment is justifiable. Compagnie des Alpes recently secured a new 25-year concession for La Plagne with a total backlog of €10.7 billion - and at the end of that concession, all infrastructure reverts to the commune. The private operator has no incentive to defer maintenance. They have to hand it all back in working order.

In Switzerland, many major operators are effectively community-owned. Zermatt Bergbahnen is essentially owned by the community that depends on it. The equity has one job.

Worth noting: the North American private operators - Alterra, Boyne, POWDR - behave considerably more like European operators than Vail does. Alterra is spending an estimated $490 million annually in capex, roughly 20-25% of revenue, funded through debt with no dividend obligation. Their Ikon Pass for 2026/27 is priced at $1,399, which is $310 more than Vail's Epic Pass - and the market is absorbing that premium. When the question is why American resorts don't invest, the precise answer is that Vail Resorts doesn't invest. Not the entire industry.

Why year-round revenue changes every calculation

The most important structural insight in this comparison doesn't show up in any winter-season analysis. Many of Europe's highest-cost new lift installations aren't being justified on skiing economics at all.

When Jungfraubahn built the Eiger Express 3S gondola in 2020 at around half a billion dollars, the primary justification wasn't moving more skiers. It was summer sightseeing traffic and faster access to the Jungfraujoch cog railway, which has been running since 1912 - before either World War, before commercial aviation, before most of the ski resorts that now benefit from the same infrastructure were even conceived. The ski season is almost incidental to that business.

The Matterhorn Alpine Crossing, which opened in July 2023 at an estimated CHF 140-200 million, connects Zermatt and Cervinia at 3,883 metres and operates year-round. Zermatt Bergbahnen projects CHF 40 million in annual income from this crossing alone - roughly a 23% annual return on capital - because it runs in summer at premium prices to an international sightseeing market prepared to pay CHF 156 for a one-way crossing. That's a ski lift generating a 23% yield. Because it's not really a ski lift.

Compare that to a new chairlift in Colorado. Similar capital cost. Runs November to April. Carries skiers who already paid a flat-fee pass and aren't generating any incremental per-ride revenue. The return on investment calculation is an entirely different exercise.

Switzerland's cable car industry generated CHF 1.8 billion in total revenue in 2025. Summer transport revenue has grown 260% since 2008; winter transport grew 23% over the same period. The industry now earns roughly CHF 360 million annually from summer transport - around 20% of total and still growing.

How the Jungfraubahn earns most of its revenue and where it invests.

Jungfraubahn's own accounts make the point with uncomfortable clarity. Their summer sightseeing segment generated CHF 56.1 million in revenue and CHF 36.7 million in EBITDA - a 65% operating margin. Their ski segment generated CHF 42 million in revenue and CHF 4.8 million in EBITDA - an 11% margin. Summer was 7.6 times more profitable than winter on a per-revenue basis. At Jungfraubahn, skiing is close to a loss-leader for the sightseeing product.

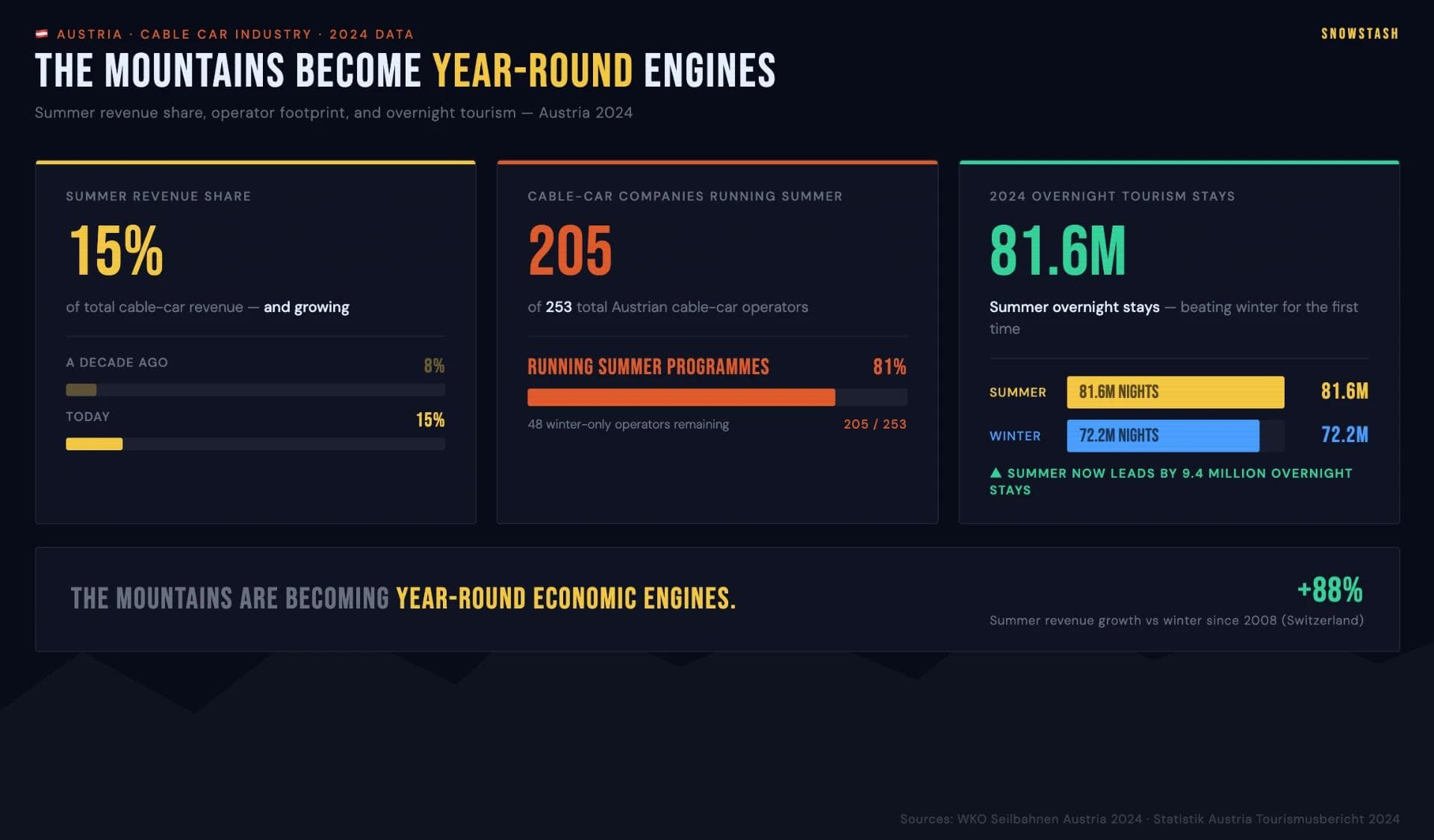

Austria's summer mountain revenue has grown from around 8% of total to roughly 15% over the past decade, with 205 of the country's 253 cable-car companies now running summer programmes. Austrian summer tourism in 2024 recorded 81.6 million overnight stays - ahead of winter's 72.2 million.

Austria also now earns a larger portion of their revenue from Summer Tourism.

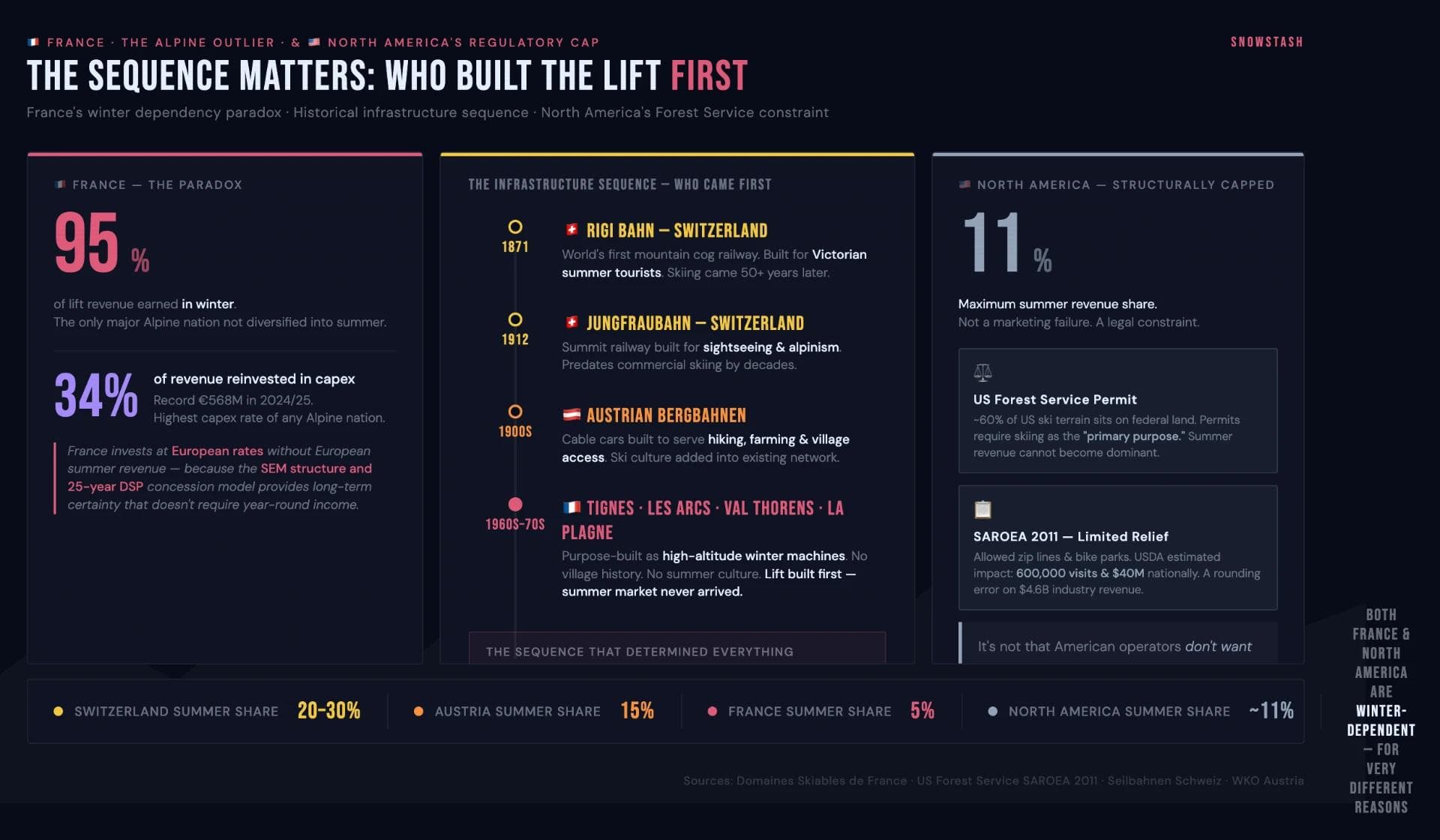

France remains the notable exception, earning around 95% of lift revenue in winter, but achieves its 34% capex rate through the certainty of long-term concessions rather than diversified revenue.

North America is structurally held at around 11% summer revenue - and it isn't for want of trying.

France and North America make no where near the same income from summer tourism.

The regulatory architecture holding North America back

Roughly 60% of American ski terrain sits on US Forest Service land, under permits whose primary purpose must legally remain skiing. The Ski Area Recreational Opportunity Enhancement Act of 2011 technically permitted zip lines, mountain bike parks, and summer activities - but the USDA's own estimate for the entire national impact of that legislation was 600,000 extra visits and $40 million in additional spending. In an industry generating $4.6 billion annually, that registers as statistical noise.

As of March 2026, a proposed Federal Register change would eliminate the Forest Service's "preponderance of revenue" test for ski areas - an acknowledgment, at the regulatory level, that the existing framework has been actively preventing meaningful summer diversification. Whether it passes or not, the acknowledgment itself is significant.

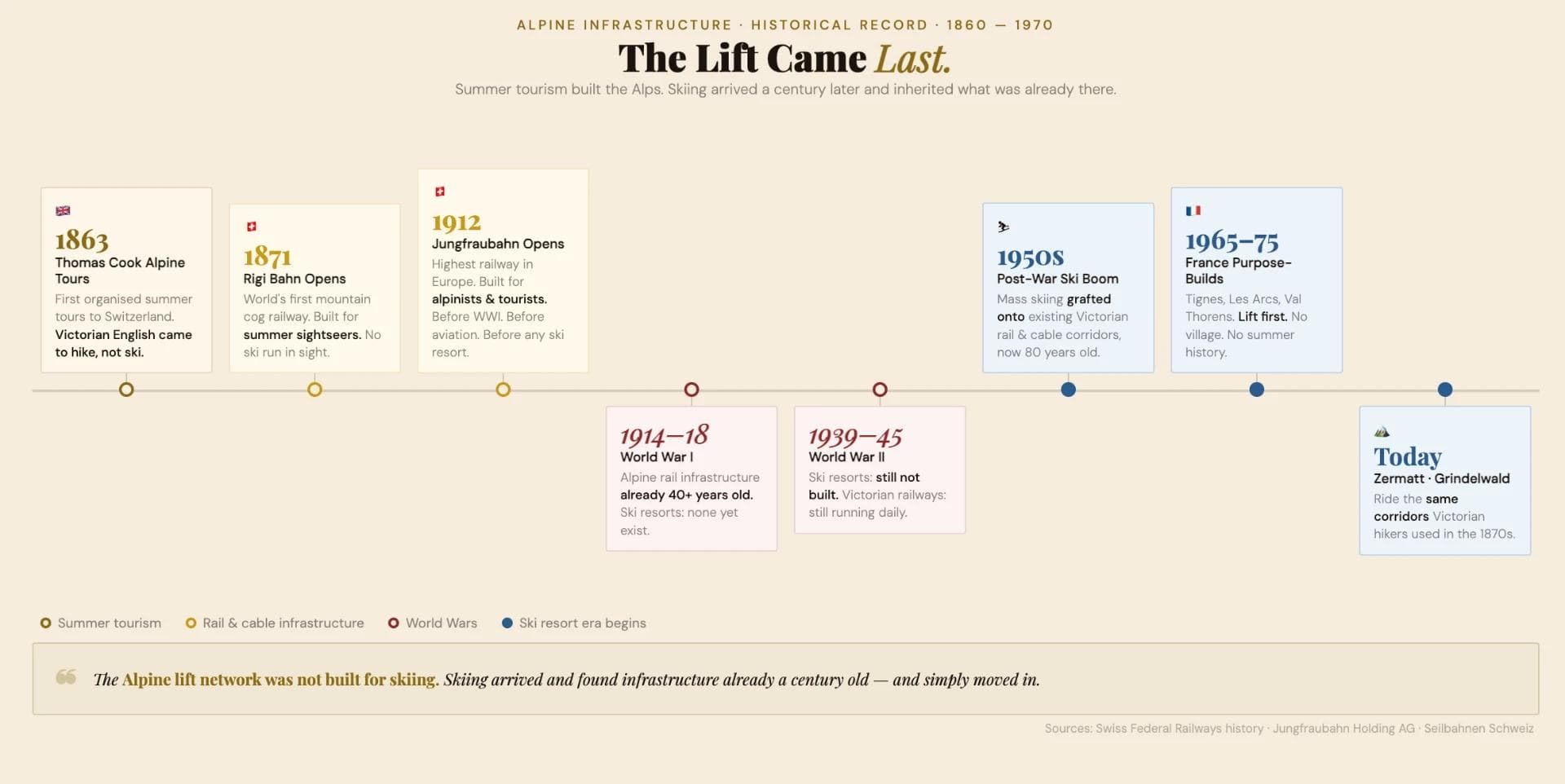

Looking back at where it all started in the Alps before people were skiing.

But regulatory permission alone wouldn't close the gap. European summer mountain tourism wasn't created by policy. It exists because Switzerland, Austria, and parts of Italy have had summer Alpine tourism culture since the 1860s and 1870s. The Rigi cog railway opened in 1871. Visitors were coming to the Alps to hike, climb, and paint the scenery before mass skiing existed anywhere. The network of hotels, trains, cable cars, and cog railways was built for that summer market. Skiing arrived later and grafted itself onto infrastructure that already had a reason to exist twelve months a year.

Whistler Blackcomb is the most useful North American data point here. The continent's most successful summer mountain operation, with around 100 kilometres of lift-served mountain bike trails and the annual Crankworx festival, still generates summer visits at roughly 30% of winter - translating to around 10-15% of revenue. Because summer yield per visit is dramatically lower than ski season. Cyclists aren't buying $250 lift tickets plus $35 lunches plus equipment rental. Whistler is the exception that shows why the European model requires both regulatory permission and 150 years of cultural groundwork beneath it.

When the lift is the actual road

There's one dimension to European lift investment that has no North American equivalent, and I think it explains more than any financial analysis.

In Switzerland, a cable car is federally regulated public transport infrastructure - governed under the same legal framework as the national rail network. Concession holders are integrated into the SwissPass and national ticketing system alongside SBB trains. Your Swiss GA annual travelcard covers the Wengernalpbahn, the Bergbahn Lauterbrunnen-Mürren, and the Aletsch Arena gondolas at no additional cost. For infrastructure serving as the only access to a community, the federal regional passenger transport system provides grants - not loans - covering 50% of qualifying infrastructure costs.

The reason Switzerland subsidises cable cars at this level is straightforward: some of them aren't optional infrastructure. They are the only road.

Zermatt has nearly 6,000 permanent residents and no road connection for private vehicles. Every resident, every delivery, every emergency vehicle travels by train. Saas-Fee banned private cars by municipal vote in 1951; the gondola from Saas-Grund is the community's transit system. Wengen, Mürren, and Gimmelwald are accessible only by cog railway and cable car - communities of 1,300, 450, and 130 residents respectively. The Aletsch Arena villages of Bettmeralp and Riederalp are gondola-only; every loaf of bread, every school pupil, every construction beam travels by cable car. In Italy's Aosta Valley, the comune of Chamois - population 111 - voted 95% against building a road in a 1965 referendum. Their cableway runs every 15-30 minutes from 7am to 10:30pm, seven days a week. It is not a ski lift. It is a road.

When you understand that context, the Swiss average of $16.75 million per new lift installation makes immediate sense. You build it to last. You build it reliably, in all conditions, for all seasons. You don't defer the maintenance cycle because a CFO wants a larger buyback programme. And the Austrian federal cableway law explicitly notes the role of cable cars in supporting jobs in rural areas - mountain access as public interest isn't a slogan there. It's written into federal legislation.

North American ski lift operators receive none of this. No public co-funding, no integration into a national transport network, no community access mandate. The lift exists to carry skiers. That is the beginning and end of its purpose.

Signs the market is starting to notice

Vail's Epic Pass recorded its first unit decline in the 2024/25 season - down 2% on the prior year. For a product that grew from 650,000 units in 2016-17 to 2.3 million in 2022-23, that inflection is worth paying attention to.

Vail's Resort EBITDA has been essentially flat across four consecutive years: $836.9 million, $834.8 million, $825.1 million, $844.1 million. Revenue grew $79 million across that period. The margin is compressing.

Alterra, meanwhile, is investing at European-scale rates and posting stronger pass growth, with the Ikon Pass commanding a $310 premium over the Epic Pass that the market is absorbing. That premium is a revealed preference for infrastructure quality. Guests can feel the difference between a resort that has been consistently reinvested in and one that hasn't - even if they couldn't write a word of financial analysis explaining why.

In March 2026, a class action antitrust lawsuit was filed alleging that the Epic Pass and Ikon Pass together constitute anticompetitive bundling that reduces the pressure on either operator to invest in the guest experience. Speculating on the legal merits isn't useful here - but the fact that it was filed reflects something real about where sentiment sits.

On the European side, the 2024/25 season set records. Austria reached €2.0 billion in lift revenue on 51.9 million skier days - both all-time highs. France hit 54.8 million skier days and a record €568 million in capex. Switzerland logged 26.3 million skier days, its strongest in 15 years. Zermatt Bergbahnen crossed CHF 100 million in revenue for the first time, with record summer first entries of 674,000. That last number - 674,000 summer entries at a ski resort - is itself the entire argument. Record revenues being converted directly into record infrastructure investment.

What closing the gap would actually require

Three things would need to change for North America to meaningfully close this gap. None of them are quick.

The first is reduced shareholder return obligations. Vail's $265 million FY25 buyback equalled its entire mountain capex budget. If the Epic Pass plateau persists, the board will eventually face pressure to rebalance allocation toward investment. It's a plausible outcome - but it requires a deliberate choice against short-term shareholder preferences that boards of listed companies don't make easily.

The second is regulatory flexibility on Forest Service land. The proposed 2026 Federal Register change is the most consequential potential unlock in North American ski history. Without it, roughly 60% of US ski terrain remains legally constrained to winter operations. With it, resorts could begin building investment cases on year-round revenue - which, as established, changes everything about what's financially justifiable.

The third is the hardest: the cultural and geographic foundation doesn't exist. Whistler functions as a summer destination because Whistler Village predated the ski resort, because it sits 90 minutes from Vancouver along a coastal mountain corridor already used by hikers and cyclists, and because it has three decades of reputation-building behind it. Most US ski areas are winter communities that go quiet in April. Building meaningful summer visitation from scratch, with no pre-existing cultural memory of mountain recreation in July, is a decade-plus project under the most optimistic scenario.

Deer Valley's East Village expansion - a $3.2 billion mixed-use, year-round development designed with the European integrated-destination model in mind - is the most serious North American attempt to test whether that gap can be closed by investment alone. If it works, it becomes the blueprint.

The underlying reason

The question was why North American ski resorts don't invest in lifts like Europe does.

The structural answer involves three overlapping problems: a listed operator whose governance model prioritises shareholder returns over mountain investment, a regulatory framework that caps year-round revenue potential, and the absence of the 19th-century summer mountain culture on which European year-round economics were originally built.

What North America is up against to close the gap.

The shareholder return problem is the most solvable - it's a capital allocation choice, and sustained commercial pressure can force it. The regulatory problem is actively being addressed. The cultural and geographic problem is the one that doesn't respond to either board decisions or legislation, and it's the one that will determine whether anything else actually sticks.

But underneath all of that structural analysis is something simpler. European operators invest in lifts because European lifts were built to serve the mountain - the communities that depend on them, the hikers who were there long before skiing existed, the residents who have no other way in or out. When a gondola is the only road into your town, the question of whether to maintain it properly isn't a financial calculation. It's a basic obligation.

The ski product, in much of the Alps, is a secondary beneficiary of infrastructure that exists for deeper reasons. North America built its lift networks specifically and exclusively for skiing. And that original design decision is still shaping every investment calculation made today.

The 2025/26 database: 3.4 times more investment in the Alps than in North America. The next time you're queuing for a fixed-grip quad at a major US resort that charged you $250 to walk through the gate, that's the number.