Why a Lift Ticket Costs $356 at Vail and €76 in Austria - And Almost Nobody Pays the American Price

Published Date:

Melbourne-based skier and snowboarder with 50+ resorts across 5 continents. Specialises in Australian resorts and international resort comparisons.

A lift ticket at Vail Mountain hit $356 US this season - and almost nobody paid it

If you'd rather watch this one, the full video breakdown is below and covers the same ground in more depth. If you're reading on, here's the short version - and then the long one.

Three-quarters of visits to Vail Mountain last season came from Epic Pass holders, according to a Vail Resorts spokesperson's own statement to the Vail Daily in December 2024. Nationally, season-pass and frequency-product visits combined accounted for around 68% of all US skier visits in 2024-25, per the NSAA's Kottke End of Season Report. The $356 window rate is closer to a manufacturer's suggested retail price than a number anyone actually hands over at the ticket window.

That reframes the question. It's not really "why is skiing this expensive in America." It's "why did an entire industry build a pricing system where the sticker price is designed to be avoided" - and why, a few thousand kilometres away, a walk-up ticket in Europe still costs around €76 with no pass required at all.

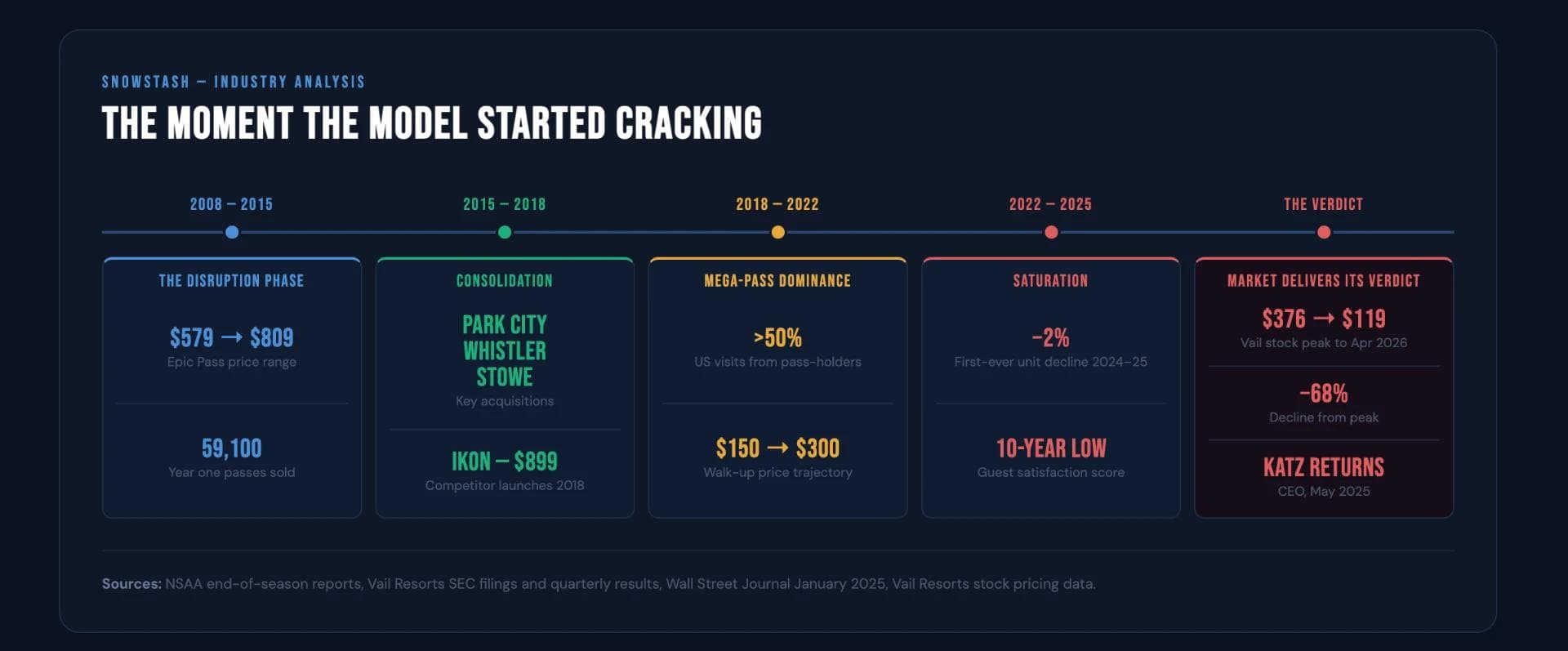

How One Company Turned Skiing Into a Subscription

The man who built the pricing system says he built it on purpose

Rob Katz, the Vail Resorts CEO who launched the Epic Pass in 2008 and returned to the role in May 2025 after his successor departed following several missed quarters, has been unusually direct about the strategy behind it. In an interview with the Storm Skiing Journal podcast, Katz said: "We had to make lift tickets absolutely expensive because we wanted people to move from lift tickets to the pass." That's not a company defending an awkward number to a journalist. That's the architect of the system explaining, on the record, that the walk-up price was never meant to reflect what a day of skiing costs - it was built to make the alternative feel unbearable.

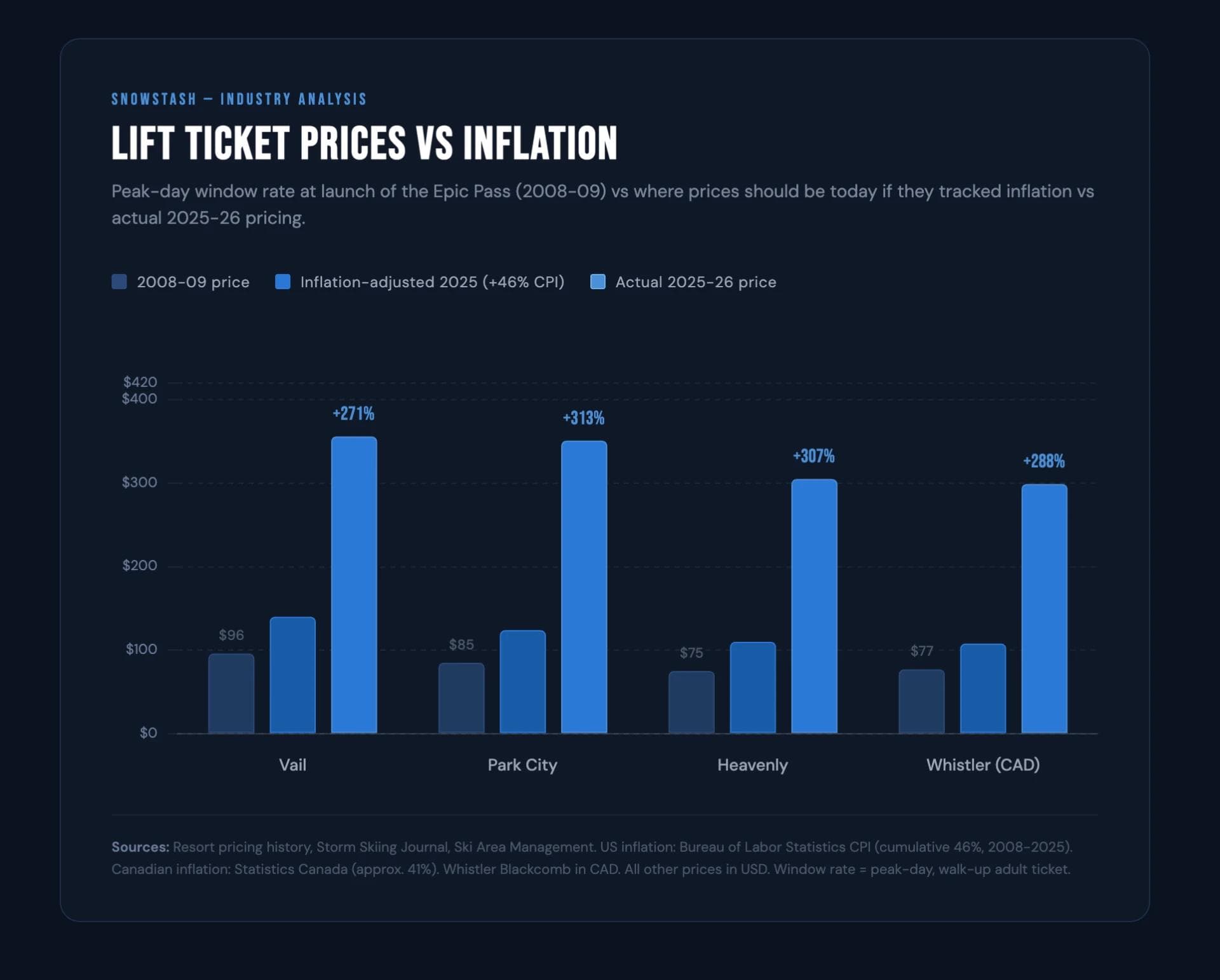

The numbers back him up. Vail Mountain's peak-day window rate was around $95 in 2008-09, the same season the Epic Pass launched. Adjusted for inflation, that ticket should sit somewhere around $115-140 today. It costs $356.

This graph demonsrates where the pricing was, where it should be with inflation vs where it really is.

Meanwhile the Epic Pass itself, in real terms, has barely moved - $579 at launch, $1,089 for 2026-27, a period across which the general cost of living rose by roughly the same proportion. The pass got relatively cheaper. The door beside it got dramatically more expensive. That gap is the strategy.

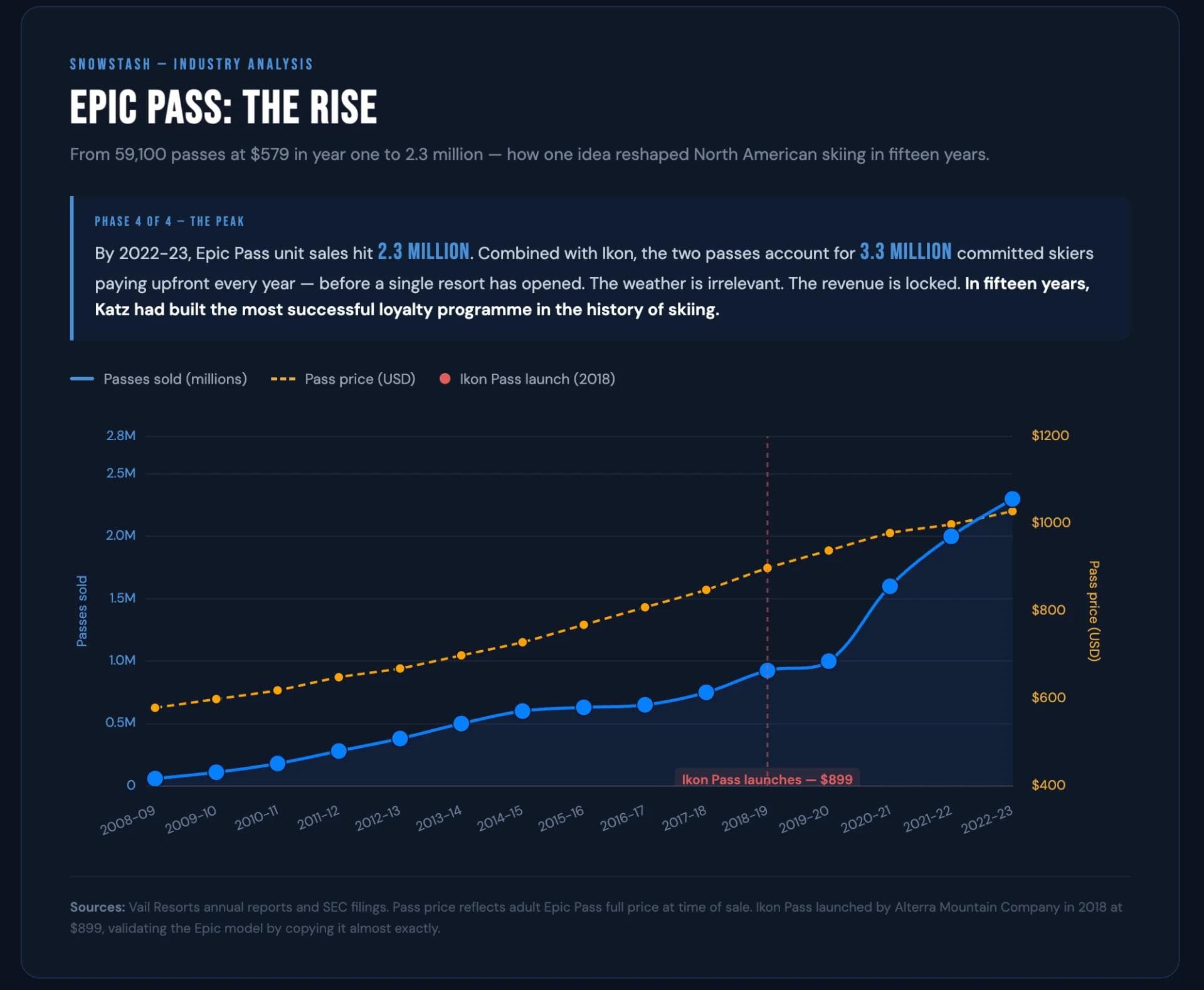

The gradual rise of the Epic Pass Pricing against the volume of pass sales.

Where the Epic Pass money actually goes

The Epic Pass didn't just change how people buy lift access - it funded a buying spree. Park City in 2014. Whistler Blackcomb in 2016, at $1.1 billion US the largest ski resort acquisition in history. Stowe in 2017. Peak Resorts' 17 mountains in 2019. Then Australia: Perisher in 2015, followed by Falls Creek and Hotham in 2019, giving Vail three of the largest lift networks in the Southern Hemisphere. Then into Europe: a 55% stake in Andermatt-Sedrun in 2022, Crans-Montana in 2023. Publicly disclosed acquisition spending between 2014 and 2023 crossed $2.5 billion, financed mostly by debt.

That debt now sits at roughly $2.7 billion against Resort EBITDA of around $825 million - about 3.3 times leverage - and servicing it shapes almost every pricing decision that follows. In FY2025, Vail returned close to $595 million to shareholders through dividends and buybacks, against approximately $225 million spent on mountain capital investment. Resort EBITDA margin, meanwhile, has compressed from 33.2% in FY2022 to around 28.6% as labour and energy costs outpace ticket revenue growth.

Timeline showing the major acquisitions by Vail Resorts and their pricing.

None of that means Vail isn't investing at all - the wider US industry, Vail included, put a record $754 million into lifts and infrastructure in 2023-24, with 97 new or upgraded lifts installed that year. But the shareholder-return-to-mountain-capex ratio tells its own story about where a $2.7 billion debt load pulls the incentives.

The other side of the ledger - what actually costs more in America

It would be too simple to say the entire price gap is financial engineering. Genuine cost differences exist, and they're worth naming honestly. US ski areas on Forest Service land pay a graduated permit fee that reaches 4% of revenue above $50 million - a cost European resorts on communal or private land simply don't carry. Liability exposure is another: a Denver jury awarded $21 million (reduced to $12.4 million under Colorado's damages cap) against Vail Resorts in 2025 over a chairlift injury at Crested Butte, and the Colorado Supreme Court has ruled that liability waivers don't shield operators who breach state safety statutes. In Austria, Italy, France and Switzerland, by contrast, skiers themselves typically carry mandatory third-party liability cover for €8-20 a trip, capping the operator's own exposure. Add US labour and housing costs in resort towns where median home prices have decoupled from local wages, and it's reasonable to estimate that genuine cost differentials explain somewhere in the order of $30-50 of the gap between a US and European lift ticket.

They don't explain the other $100-200. That remainder is pricing power - the product of an industry where one operator now accounts for roughly a quarter of all North American skier visits, largely removing the competitive pressure that would otherwise keep a window rate honest.

It's also worth noting the gap exists inside North America too. Aspen Skiing Company, which has stayed outside the Epic and Ikon consolidation, prices its flagship mountain around $80 below Vail Mountain despite comparable positioning. And a small but growing tier of independents - Wolf Creek at $97, Mad River Glen at $109, Bogus Basin at $89 - never joined a mega-pass network at all, and their prices sit almost exactly where an inflation-adjusted 2008 ticket should. The Indy Pass, built explicitly as what its founder calls the "anti-mega-pass," has grown from around 50 partner resorts in 2019 to 271 today by selling access to exactly that tier at roughly 30% of an Ikon Pass's price. The independents aren't underpricing the market. The majors overshot it.

Why Europe never built this system

A skier in Salzburg doesn't need to think about corporate ownership structures to notice that a day at any one resort costs about the same as a day at the one down the road. That's not an accident - it's a function of how European lift networks are owned. Most are run under time-limited public-service concessions granted by local communes, typically for 20-30 years, then competitively re-tendered. Compagnie des Alpes, the largest operator in the French Alps, holds concessions on resorts including La Plagne, Val d'Isère and Méribel - but holding one isn't guaranteed forever.

Mayrhofen is home to endless terrain all accessible for €76

CDA lost its Tignes concession in 2024, handing back roughly €103 million of lift infrastructure to a newly formed local public company. It won the La Plagne renewal in late 2025, a 25-year, €5 billion contract - but only by bidding competitively against Vail Resorts, which also pursued that concession and lost. Vail's own attempt to test whether its pricing model travels to Europe has, so far, run directly into a system that caps how far outside capital can roll up the industry.

The financial outcomes are counterintuitive. CDA's ski division posted a 36.7% EBITDA margin in the first half of 2024-25 - meaningfully higher than Vail's 28.6% - while generating roughly €42 per skier day against Vail's $75. CDA converts more of a smaller number into profit partly because it doesn't carry the lodging and food and beverage operations that weigh on Vail's margins, and partly because French nuclear-backed electricity contracts kept energy costs down 17.8% in the same half-year. A €82 Trois Vallées day pass also buys access to 600 kilometres of connected terrain across three resorts - the kind of interconnected "ski circus" that would require several separate tickets at separate resorts in North America.

Japan - the market where the mega-pass has no leverage

Japan tells a different but related story. Its domestic ski market collapsed from around 18.6 million skiers at its 1993 peak to roughly 4.6 million by 2023, and the number of operating resorts fell from close to 1,700 to 449. The operators left standing are mostly railway companies and property developers for whom the lift ticket is a side note - Tokyu owns Niseko Grand Hirafu largely to drive off-peak rail demand, and the real money in Niseko is made on condominium sales to foreign buyers. Into that collapsed, low-margin market has come a wave of foreign skiers drawn by a weak yen and genuinely excellent snow: foreign visitation was up 33% on pre-pandemic levels in winter 2024-25.

Driving up to the base of Furano ski resort in Hokkaido.

A Niseko United day pass runs around ¥10,500, or roughly $69 US. Neither Vail nor Alterra has the domestic scale to reshape that pricing the way the Epic model reshaped North America - both include Japanese resorts as pass partners, but partnership hasn't come with pricing power.

Australia and New Zealand - the same season, the same skiers, two different owners

If Japan shows what happens when there's no consolidator with enough scale to try the Epic model, Australia and New Zealand show what happens when one operator does and doesn't. It's about as close to a controlled experiment as this industry gets: same hemisphere, same winter, the same pool of Australian and Kiwi skiers deciding where to spend their season - and one side of the Tasman has Vail Resorts, and the other doesn't.

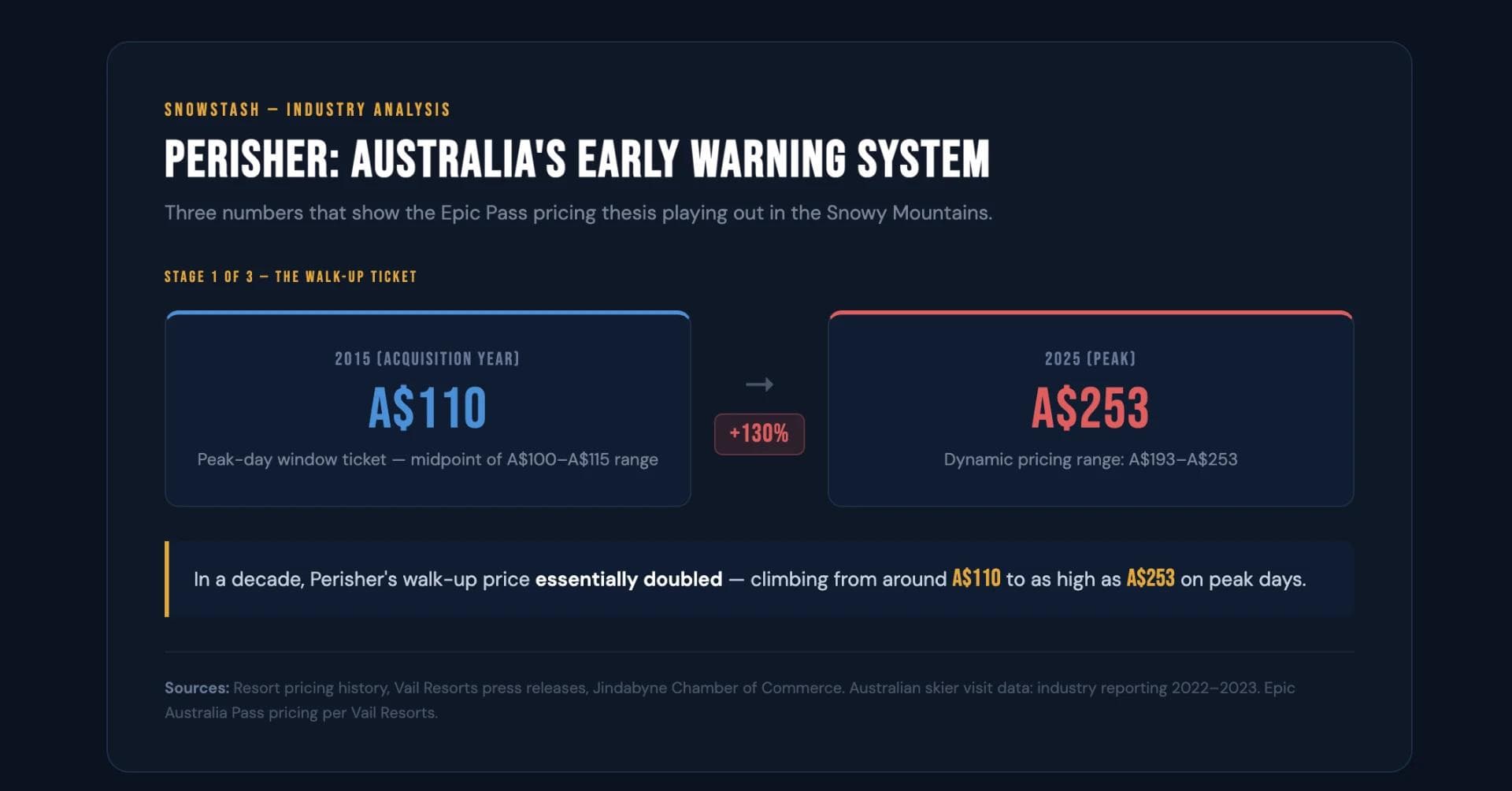

Vail bought Perisher in 2015, then Falls Creek and Hotham in 2019, taking control of three of the largest lift networks in the Southern Hemisphere. Perisher's window rate has followed a trajectory that will look familiar by now: a widely reported comparison put the resort's 1990 day-ticket price at $46, which the Reserve Bank of Australia's own inflation calculator puts at somewhere around $107-118 in today's terms.

The actual 2025-26 walk-up price runs A$193-253 depending on the date - roughly double what a straight inflation adjustment would produce, tracking almost exactly the North American pattern. The Epic Australia Pass followed the same staged-scarcity mechanic as its northern hemisphere counterpart: on sale at A$1,045 for 2026 at its lowest early-bird window, climbing through a series of deadlines toward A$1,285 and beyond as the season approaches.

The Jindabyne Chamber of Commerce has been blunt about the effect. Its president, Olivier Kapetanakos, told regional media that for a family of five with school-age kids, "it's probably cheaper to go overseas" than to ski the Snowy Mountains. Australian skier visits fell from roughly 2.59 million in 2022 to 1.93 million in 2023, a decline of about 26% - though it's worth being fair to the data here: 2023 was also a genuinely poor snow season, with Perisher Valley recording its warmest July in over a decade, so pricing is one factor in that drop rather than the sole cause.

Mt Buller took a different path. Victoria's largest lift network stayed independent, joining the Ikon Pass network and the Mountain Collective rather than selling to Vail, and prices accordingly - its 6 Day Any Day pass runs A$849 for 2026, positioning it inside the Australian market roughly the way Aspen Skiing Company sits inside the American one: comparable terrain, deliberately outside the consolidation.

Cross the Tasman and there's no Vail presence at all. NZSki's Superpass, covering Coronet Peak, The Remarkables and Mt Hutt, runs NZ$105 a day; Cardrona and Treble Cone sit in the NZ$100-165 range. In practical terms that's meaningfully below Perisher's window rate, in a market with no Epic-style consolidator to push it upward. And Australians have noticed: NZSki reported Australian visitor numbers up almost 14% in 2024 on the year before - a real, measurable substitution effect showing up in the exact place the pricing theory predicts it should. Layer on top of that Australia's own structural headwind - modelling from the Australian National University and Protect Our Winters projects the local season could be roughly half its current length by 2050 - and the Perisher case looks less like a one-off and more like a preview of where the North American numbers are headed if nothing changes.

The model is already showing cracks

None of this is static, and the last eighteen months have made that obvious. Vail Resorts stock peaked at $376.24 in November 2021; by late April 2026 it had fallen to $119.02, a 68% decline. Q2 FY2026 results showed revenue down 4.7% and Resort EBITDA down 8.3%, with US skier visits down around 12% season-to-date - a slide the company attributed largely to the worst Rockies snow season in more than thirty years, though pass-unit sales had already declined in each of the two prior seasons regardless of snowfall. Guest satisfaction at Vail's largest resorts hit a decade low. A Wall Street Journal cover story in January 2025 was headlined "Vail Resorts Has an Epic Problem." And in December 2024, 200 unionised ski patrollers at Park City walked out for twelve days seeking a wage increase from $21 to $23 an hour, raising over $300,000 through a GoFundMe campaign that one Wall Street analyst publicly called "concerning for the company." The strike settled at an average $4-an-hour increase.

In March 2026, four plaintiffs filed a federal antitrust class action - Goloja et al. v. Vail Resorts, Inc. et al. - in the US District Court for the District of Colorado, alleging that Vail and Alterra's parallel use of punitive window pricing to push skiers toward mega-passes amounts to anticompetitive bundling under the Sherman Antitrust Act and Colorado's own 2023 antitrust statute. Vail has called the claims without merit, pointing out that the Epic Pass cut the cost of an unrestricted season pass by 60% when it launched in 2008. The case is at the pleading stage, with no class certification and no economic evidence yet before the court - it's a signal of where the industry's temperature sits right now, not a finding of fact.

Vail's own response to the pressure has been to soften the exact mechanism Katz once described building. Late 2025 brought "Epic Friends" half-price tickets for pass-holder groups, a 30%-off discount for purchases made 30 days ahead, and a "Turn In Your Ticket" scheme letting skiers convert day-ticket spend toward next year's pass. They're not cosmetic. They're an admission that the punitive walk-up model has found its ceiling.

So who's actually right about the $356 ticket

Both the outraged headlines and the industry's own defence are true at the same time, just about different things. The headline number is a list price almost nobody pays, and pass math genuinely can bring a committed skier's cost down to $50-100 a day. But that same pricing architecture genuinely does shut out first-timers, casual visitors, and anyone who can't or won't commit several hundred dollars months in advance - and that's not an accident either, on Rob Katz's own account.

The real story is that three things happened at once. A brilliant subscription model launched in 2008 and worked exactly as designed. The debt raised to fund a decade of acquisitions built off that model's success created financial pressure that now shows up in shareholder payouts, executive pay, and a window rate used as a conversion tool rather than a real price. And the mechanism built to herd committed skiers onto passes became, for everyone outside that ecosystem, a closed door. Europe never built the second and third parts because its ownership model doesn't allow the debt-fuelled version of the first. Japan never built any of it because its domestic market collapsed before anyone had the scale to try. And Australia and New Zealand, sitting side by side in the same hemisphere, ended up as the cleanest real-world test of the whole theory - one bought by the consolidator, one not, with the pricing and the visitor numbers moving exactly the way the theory predicts on both sides of the Tasman.

Whether the current pullback comes fast enough to hold the audience North American skiing spent fifteen years building - or whether enough of that audience has already done the Japan, Europe or New Zealand maths and found it a better trip - is the question the industry is now answering in real time, one earnings call and one lawsuit at a time.

The full video goes further into the acquisition timeline resort by resort, the mechanics of the Epic and Ikon pass math, and what all of this means if you're planning a 2026-27 season trip. It's below - worth fifteen minutes if you want the whole picture.